Leveraging the Self-Employment Retirement Advantage

Being your own boss comes with incredible freedom – setting your own hours, choosing your clients, and building something that’s truly yours. But let’s face it, that freedom comes with a retirement planning challenge. Without an employer dropping those regular 401(k) contributions into your account, you’re on your own.

Or are you?

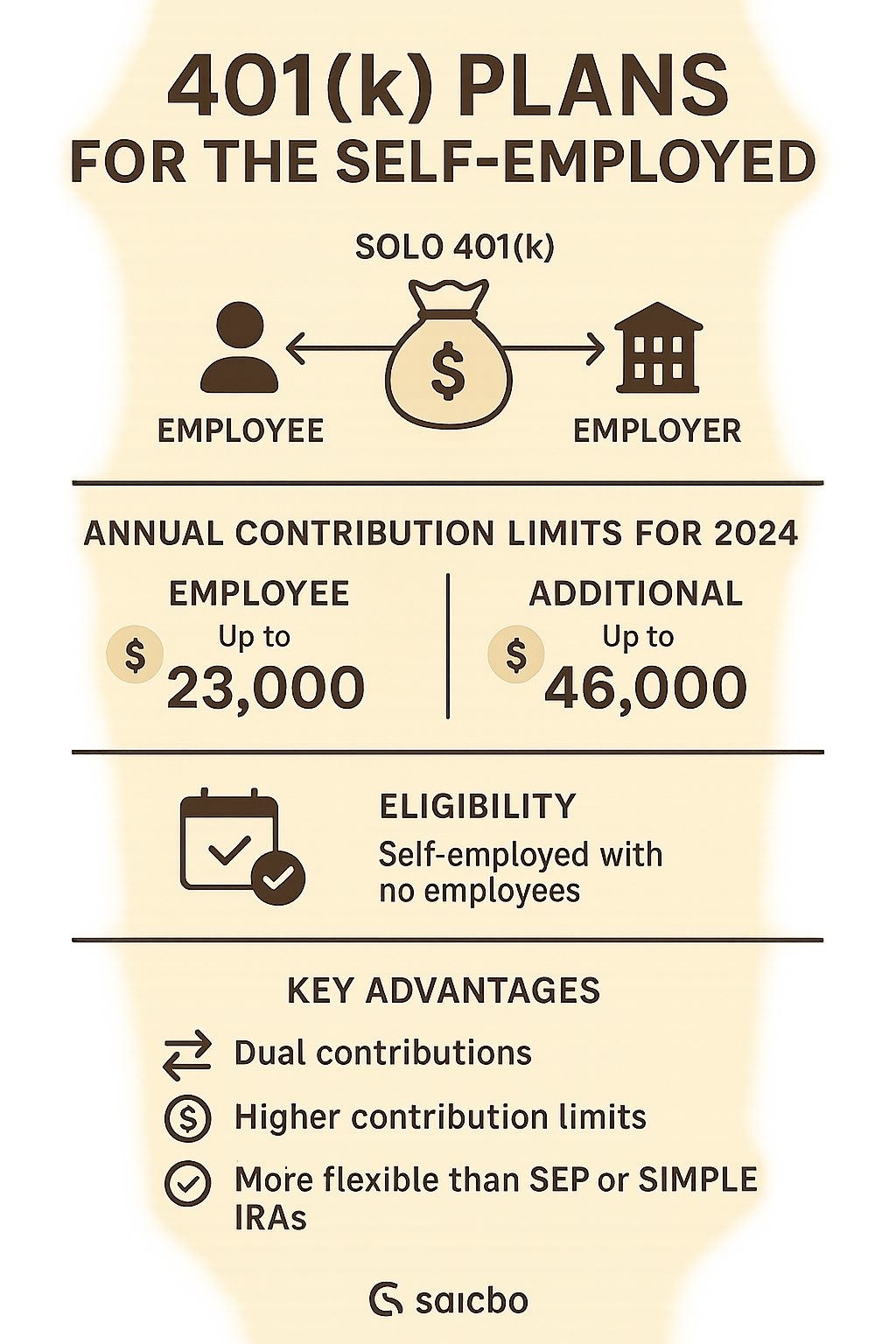

401k plans for self employed individuals actually offer a hidden superpower that traditional employees don’t get: the ability to wear two hats when saving for retirement. As both “employee” and “employer,” you can contribute significantly more than the average worker.

Think of it as your reward for handling everything from client service to accounting to marketing all on your own!

These specialized retirement accounts (sometimes called solo 401(k)s, individual 401(k)s, or one-participant plans) are specifically designed for business owners with no employees – or just a spouse working in the business. The beauty lies in their flexibility and generous contribution limits.

In 2025, you can set aside up to $23,500 in employee salary deferrals. But here’s where it gets interesting – you can also make an additional employer contribution of up to 25% of your compensation (with some calculation adjustments for sole proprietors). This powerful combination allows for total contributions up to a whopping $69,750, or $77,500 if you’re 50 or older thanks to catch-up provisions.

Another perk? These plans involve minimal paperwork compared to their corporate cousins. You only need to file Form 5500-EZ annually once your plan assets reach $250,000.

Here’s a quick overview of your options:

| Type of Solo 401(k) | Best For | 2025 Contribution Limit |

|---|---|---|

| Traditional Solo 401(k) | Those wanting immediate tax deductions | Up to $69,750 ($77,500 if 50+) |

| Roth Solo 401(k) | Those expecting higher future tax rates | Same limits, but with tax-free withdrawals in retirement |

| Self-Directed Solo 401(k) | Those wanting alternative investments | Same limits, with broader investment options |

| Low-Cost Index Solo 401(k) | Those prioritizing simplicity and low fees | Same limits, typically lower ongoing costs |

What makes 401k plans for self employed particularly versatile is their flexibility with contribution types. Unlike SEP IRAs, you can choose traditional pre-tax contributions (reducing your current tax bill), Roth after-tax contributions (for tax-free growth), or even a strategic mix of both.

Self-employment means wearing many hats – but when it comes to retirement planning, those multiple hats actually work in your favor!

What Makes 401(k) Plans for Self-Employed Unique

The beauty of 401k plans for self employed individuals lies in their extraordinary dual-contribution structure. When you work for yourself, you’re not just the employee—you’re also the boss! This double identity creates a retirement savings superpower that employed individuals simply don’t have.

As both employee and employer, you can contribute from two directions:

- Your “employee hat” allows you to set aside up to $23,500 for 2025 through salary deferrals

- Your “employer hat” lets you add up to 25% of your compensation (which works out to roughly 20% of net self-employment income for sole proprietors)

This powerful combination creates one of the highest contribution ceilings in the retirement planning world. It’s like having access to two gas pedals when saving for your future!

To qualify for this retirement powerhouse, you need to:

– Have income from self-employment activities

– Have no common-law employees (those working more than 1,000 hours annually)

– Be running your business as a sole proprietor, LLC owner, partnership member, or corporation owner

“The solo 401(k) is truly the heavyweight champion of retirement plans for the self-employed,” as one financial advisor puts it. “Dollar for dollar, it allows higher combined contributions at identical income levels compared to other self-employed plans.”

Another fantastic feature not available with all retirement plans is the ability to take loans. Many solo 401(k) plans allow you to borrow up to 50% of your balance (maximum $50,000) without taxes or penalties, as long as you stick to the repayment schedule. This flexibility can be a lifesaver during cash crunches—something every self-employed person understands all too well.

For deeper insights into establishing and managing these plans, check out the Department of Labor’s comprehensive guide: 401(k) Plans for Small Businesses PDF.

401k plans for self employed vs. SEP & SIMPLE

When shopping for the right retirement vehicle, 401k plans for self employed individuals often race ahead of the competition, especially if maximizing your savings is the goal. Let’s see how they compare to other popular options:

| Feature | Solo 401(k) | SEP IRA | SIMPLE IRA |

|---|---|---|---|

| 2025 Max Contribution | $69,750 ($77,500 if 50+) | $69,750 | $19,750 ($23,500 if 50+) |

| Employee Deferrals | Yes, up to $23,500 | No | Yes, up to $16,500 |

| Employer Contribution | Up to 25% of compensation | Up to 25% of compensation | Required (3% match or 2% non-elective) |

| Roth Option | Yes | No | No |

| Loan Provisions | Available with many plans | Not available | Not available |

| Administration | Simple until assets reach $250,000 | Very simple | Simple |

| Best For | Maximizing contributions | Simplicity with high contribution potential | Small businesses with employees |

The math tells a compelling story about why solo 401(k)s often win the retirement race. Picture this real-world example:

Imagine you’re a self-employed graphic designer earning $100,000 in net self-employment income in 2025. Your contribution options would look like:

With a solo 401(k), you could save $23,500 as an employee plus approximately $20,000 as the employer, totaling a whopping $43,500 toward retirement. That’s 43.5% of your income!

With a SEP IRA, you’d be limited to about $20,000 (employer contribution only).

With a SIMPLE IRA, you could save $16,500 as an employee plus $3,000 as the employer, totaling $19,500.

At this income level, the solo 401(k) allows you to save more than twice what a SEP IRA would permit—a difference that could mean hundreds of thousands of dollars over your career.

Another game-changing advantage is the Roth option. Solo 401(k)s can include Roth contributions for the employee portion, giving you the gift of tax-free growth and withdrawals in retirement—something SEP IRAs simply don’t offer.

Key 2025 numbers for 401k plans for self employed

For 2025, here are the magic numbers you need to know for your 401k plans for self employed planning:

Your employee deferral limit sits at $23,500 (whether pre-tax, Roth, or some of each). If you’re 50 or older, you get an extra $7,500 catch-up contribution—because it’s never too late to boost your retirement savings!

As the employer, you can contribute up to 25% of your compensation (which translates to about 20% for sole proprietors). All told, your combined limit reaches an impressive $69,750, or $77,500 if you’re 50+. Just remember that when calculating contributions, the IRS only considers the first $350,000 of compensation.

The SECURE 2.0 Act has brought some welcome improvements to the retirement landscape:

- If you’re between 60-63, you’ll see increased catch-up contribution limits in 2025

- Employers now have the option to make matching contributions as Roth contributions

- The Required Minimum Distribution (RMD) age has increased to 73 and will rise to 75 by 2033

These changes reflect the government’s recognition that Americans are working longer and need more flexibility in their retirement planning—especially those of us navigating self-employment.

2025 Contribution & Tax Rules at a Glance

When you’re juggling client work and business operations, understanding the nuts and bolts of your 401k plan for self employed individuals might feel like one more task on your never-ending to-do list. But these rules are actually your secret weapon for building wealth while managing your tax bill.

Let’s break down the 2025 contribution rules in plain English:

As a self-employed person, you wear two hats – employee and employer. This dual identity lets you contribute significantly more than regular employees can:

As your own employee, you can set aside up to $23,500 in 2025 through salary deferrals. Then, wearing your employer hat, you can add up to 25% of your compensation on top of that. Together, these contributions can’t exceed $69,750 for 2025 (or $77,500 if you’re 50 or older).

The IRS only considers the first $350,000 of your compensation when calculating these limits. Even Elon Musk has to follow this rule!

For sole proprietors and single-member LLCs, calculating your employer contribution takes a special formula (because you don’t technically pay yourself a W-2 salary). Here’s how it works in practice:

Let’s say your business profit is $100,000 before retirement contributions. First, subtract about $7,650 (half of your self-employment tax). This gives you $92,350 in adjusted net earnings. Your maximum employer contribution would be about $18,470 (20% of that adjusted figure). Add your $23,500 employee deferral, and you could contribute a total of $41,970 to your retirement this year.

That’s a significant tax advantage while building your future nest egg! For more detailed information straight from the source, check out the Retirement Topics – 401(k) Limits page on the IRS website.

Traditional vs. Roth solo 401(k) contributions

One of the most powerful features of 401k plans for self employed individuals is the ability to choose your tax advantage. Unlike SEP IRAs, solo 401(k)s let you decide between traditional (pre-tax) and Roth (after-tax) contributions for the employee portion of your plan.

Think of it as choosing between a tax break today or tax-free income tomorrow.

With traditional contributions, you’re essentially telling the IRS “not yet” on taxes. These contributions reduce your current taxable income, which can be especially helpful during high-earning years. Your money grows without annual tax bills on dividends or capital gains, but when you eventually withdraw in retirement, you’ll pay ordinary income tax on both your contributions and earnings. Starting at age 73, you’ll need to take Required Minimum Distributions whether you need the money or not.

With Roth contributions, you’re paying your tax bill upfront. While there’s no immediate tax break, your future self might thank you profusely. All that growth accumulates completely tax-free, and qualified withdrawals in retirement won’t add a penny to your taxable income. Even better, Roth contributions aren’t subject to RMDs during your lifetime, giving you more control over your retirement tax situation.

As one of my clients recently put it: “Traditional is like buying a vacation home with a mortgage; Roth is like paying cash. You’ll enjoy the same house either way, but the experience feels very different!”

The choice often comes down to a simple question: Will your tax rate be higher now or in retirement? If you believe taxes are on sale today, traditional contributions make sense. If you think tax rates will climb or your income will be higher in retirement, Roth contributions might be the better long-term value.

Can’t decide? You’re not locked into one approach. You can split your employee deferrals between traditional and Roth in the same year (just keep the total under the annual limit). Employer contributions must always be made pre-tax, even if you go all-in on Roth for your employee portion.

For more guidance on building your retirement portfolio, take a look at our guide to Best Retirement Funds.

Catch-up contributions after age 50

If your retirement savings aren’t quite where you’d like them to be, 401k plans for self employed individuals offer a valuable second chance through catch-up contributions. Think of these as the financial equivalent of bonus time in a soccer match – a chance to make up ground when you need it most.

For 2025, if you’re 50 or older, you can contribute an extra $7,500 on top of the standard $23,500 employee deferral limit. This brings your total employee contribution capacity to $31,000. When combined with your employer hat contributions, your overall limit jumps to $77,500 for the year.

This additional $7,500 might not sound revolutionary, but it’s actually a powerful wealth-building tool. Consider a 55-year-old web designer earning $150,000 in net self-employment income. By maximizing both regular and catch-up contributions, she could set aside:

- $31,000 as employee contributions (including the catch-up amount)

- Approximately $30,000 as employer contributions

- A grand total of $61,000 in a single year

That’s serious retirement-building power! Over a decade, those additional catch-up contributions alone could grow to over $100,000, assuming a 7% annual return.

These catch-up contributions are particularly valuable if you spent your early career investing in your business rather than your retirement, if you’re in your peak earning years and want to maximize tax advantages, or if life events created gaps in your savings history.

The beauty of catch-up contributions is they acknowledge a simple truth: the path to retirement isn’t always a straight line, especially for entrepreneurs and self-employed professionals. They give you the flexibility to accelerate your savings when you’re most able to do so, helping turn “better late than never” into “right on time.”

1. Traditional Solo 401(k)

The Traditional Solo 401(k) stands as the classic version of 401k plans for self employed individuals – think of it as the reliable sedan in a showroom of retirement vehicles. It offers something many self-employed folks crave: immediate tax relief.

Here’s how it works: you contribute pre-tax dollars from your business earnings, which lowers your taxable income right now. This means more money stays in your pocket during tax season, rather than going to Uncle Sam.

Your contributions come from two separate sources, showcasing the unique dual-hat approach of solo 401(k)s:

First, as an employee of your own business, you can set aside up to $23,500 in 2025 (or $31,000 if you’re 50 or older). Every dollar here directly reduces your taxable income. Then, wearing your employer hat, you can add up to 25% of your compensation as a profit-sharing contribution (about 20% of net self-employment income for sole proprietors).

The tax savings can be substantial. If you’re in the 24% federal bracket and contribute $20,000, you could save $4,800 on your federal tax bill this year. That’s like getting paid to save for retirement!

Your money then grows tax-deferred inside the account – no taxes on dividends, interest, or capital gains along the way. The tax bill only comes due when you take withdrawals in retirement, when many people find themselves in lower tax brackets than during their working years.

That Required Minimum Distributions (RMDs) kick in at age 73, requiring you to start taking money out according to IRS formulas. Another helpful feature: many Traditional Solo 401(k) plans offer loan provisions, letting you borrow up to 50% of your balance (maximum $50,000) if life throws an expensive curveball your way.

Who should consider this 401k plan for self employed

The Traditional Solo 401(k) isn’t for everyone, but for certain self-employed individuals, it fits like a glove.

High-income earners in their peak earning years often benefit most from this plan. If you’re bringing in substantial self-employment income and wincing at your tax bill, the immediate deductions can provide welcome relief. The higher your current tax bracket, the more valuable these deductions become.

Self-employed people anticipating lower tax rates in retirement should take a close look too. If you expect to drop into a lower tax bracket after you stop working, paying taxes later rather than sooner makes mathematical sense.

Business owners with fluctuating or unpredictable income appreciate the flexibility of Traditional Solo 401(k)s. Unlike some retirement plans, there’s no requirement to contribute the same amount each year – you can adjust based on cash flow.

Late-career entrepreneurs who need to catch up on retirement savings find the high contribution limits particularly valuable. The ability to contribute both as employer and employee creates a powerful acceleration lane for retirement saving.

The Traditional Solo 401(k) offers several distinct advantages: immediate tax breaks, flexible contribution amounts, potential loan access, and strong creditor protection under federal law. Plus, you’re building a retirement nest egg that can grow substantially over time.

It’s not without drawbacks, though. Your future withdrawals will be taxed as ordinary income, early withdrawals typically trigger penalties, and you’ll face those mandatory distributions after age 73. There’s also more paperwork than some simpler plans, especially once your account exceeds $250,000.

Consider Ben, a 51-year-old independent marketing consultant earning $150,000 annually. By maximizing his Traditional Solo 401(k) with $23,500 as an employee deferral, $7,500 in catch-up contributions, and a 25% employer contribution of $37,500, he contributed a total of $68,500 in one year. This dramatically reduced his taxable income while building significant retirement savings – something that would be impossible with many other retirement vehicles.

2. Roth Solo 401(k)

The Roth Solo 401(k) stands out as perhaps the most exciting variation of 401k plans for self employed individuals who are thinking long-term about their tax situation. Think of it as trading today’s tax break for something potentially much more valuable: completely tax-free retirement income.

With a Roth Solo 401(k), you make your employee contributions (up to $23,500 in 2025, or $31,000 if you’re 50+) with after-tax dollars. While this means you won’t get an immediate tax deduction like with traditional contributions, the long-term benefits can be absolutely game-changing:

Your money grows completely tax-free for decades, and when you finally withdraw it in retirement, you won’t pay a single penny in taxes on qualified distributions. That’s right – all that growth is yours to keep!

Plus, unlike traditional accounts, Roth money isn’t subject to Required Minimum Distributions during your lifetime. This means your money can continue growing tax-free for as long as you want, giving you more control over your retirement income strategy.

It’s worth noting that the employer portion (your profit-sharing contribution) still needs to be made pre-tax under current rules. However, the SECURE 2.0 Act has introduced provisions allowing employer contributions to be designated as Roth in the future – we’re just waiting on the IRS to provide final guidance on implementation. When this happens, self-employed individuals will have the exciting option to make their entire Solo 401(k) contribution as Roth money.

Maximizing Roth space in 401k plans for self employed

The Roth Solo 401(k) isn’t for everyone, but for certain self-employed individuals, it’s practically a gift from the tax code. You might be an ideal candidate if:

You’re a young entrepreneur with decades ahead for tax-free growth. The longer your time horizon, the more valuable tax-free growth becomes.

You’re currently in a relatively low tax bracket but expect your income (and tax rate) to climb substantially in the future.

You’re concerned about future tax rate increases. With government debt growing, many financial experts believe tax rates might rise in coming decades.

You want tax diversification in retirement, giving you more flexibility in how you generate income.

Many savvy self-employed professionals use what financial planners call a “split-funding strategy.” This means dividing your contributions between Traditional and Roth accounts based on your current tax situation and future expectations.

For example, Maria, a self-employed consultant earning $120,000, might contribute $12,000 to her Roth Solo 401(k) and $11,500 to her Traditional account, plus make an employer contribution of $24,000 (pre-tax). This balanced approach gives her both immediate tax benefits and future tax-free growth.

For those looking to boost their Roth savings, the “mega backdoor Roth” strategy can be particularly powerful. If your plan allows after-tax (non-Roth) contributions beyond the standard limits, you might be able to convert these funds to Roth status, effectively increasing your Roth contribution capacity well beyond normal limits. This advanced technique isn’t available in all plans, but for those who can use it, it represents one of the most powerful tax planning opportunities available to self-employed individuals.

3. Self-Directed Solo 401(k)

The Self-Directed Solo 401(k) takes 401k plans for self employed individuals to a whole new level of flexibility. Think of it as giving yourself the keys to the investment kingdom – far beyond the typical mutual fund menu that most retirement plans offer.

With this specialized plan, you keep all the generous contribution limits ($69,750 for 2025, or $77,500 if you’re 50+), but you open up a treasure chest of investment possibilities, including:

Real estate properties that generate rental income while potentially appreciating in value. Imagine buying that apartment building you’ve always eyed, but with retirement dollars.

Private businesses and startups that could become the next big thing. That friend with the brilliant business idea? You might be able to invest in it through your retirement plan.

Private lending opportunities where you become the bank, earning interest on loans you provide to others.

Precious metals like gold, silver, platinum, and palladium – tangible assets many investors turn to during economic uncertainty.

Tax lien certificates and limited partnerships that most retirement savers never get to access.

The most powerful version – often called a “checkbook control” Self-Directed Solo 401(k) – establishes your plan with a special trust structure. This gives you the ability to make investments directly without asking a custodian’s permission for every transaction. Need to move quickly on a real estate deal? You can write a check from your plan’s account without delays.

A self-employed real estate broker I know established her Self-Directed Solo 401(k) specifically to invest in rental properties in her local market. She leveraged her industry expertise to find undervalued properties, and now the rental income flows back into her 401(k) tax-deferred. She’s essentially building a retirement plan that matches her professional knowledge.

Just remember – with great power comes great responsibility. As the plan trustee, you’re legally obligated to make prudent investment decisions and follow all IRS rules to the letter.

Guardrails to avoid costly mistakes

The freedom of Self-Directed Solo 401(k)s comes with important boundaries. Think of these as the guardrails keeping your retirement plan safely on the road and away from expensive IRS penalties.

Prohibited transactions are the biggest danger zone. The IRS strictly forbids certain activities, and breaking these rules can be catastrophic – potentially triggering taxes and penalties on your entire account balance.

The most important rules to remember:

You cannot personally benefit from plan investments outside their future retirement value. That rental property in your 401(k)? You can’t use it for weekend getaways or let your kids live there rent-free.

Transactions with “disqualified persons” are forbidden. This includes yourself, your spouse, children, parents, and certain business partners. Your Solo 401(k) can’t buy property from your parents or lend money to your daughter’s business.

Personal use of plan assets is off-limits. That beautiful beach house your 401(k) purchased must be a pure investment, not your vacation home.

Some investments are completely off the table. The IRS explicitly prohibits collectibles in all 401(k) plans – so your retirement dollars can’t go toward art, antiques, rugs, most metals (with limited exceptions for certain coins and bullion), gems, stamps, or that vintage wine collection you’ve been eyeing.

Life insurance policies are generally not allowed in 401(k) plans, with very limited exceptions.

S-Corporation stock ownership is prohibited – not by 401(k) rules, but by S-Corporation regulations themselves.

For detailed guidance on collectible restrictions, the IRS provides helpful information in their Issue Snapshot on Collectibles.

To keep your Self-Directed Solo 401(k) safe, follow these common-sense practices:

Work with a specialized provider who understands these complex plans. The mainstream brokerage you use for your personal accounts might not be the right choice here.

Document everything carefully – every transaction should have a clear paper trail.

Consider consulting with a tax professional before making unusual investments. An hour with a professional can save years of headaches.

Maintain completely separate finances between your personal life and retirement plan. No commingling of funds, ever.

Stay current on IRS rules, which can evolve over time.

While Self-Directed Solo 401(k)s require more knowledge and attention than standard retirement accounts, they offer tremendous opportunities for self-employed individuals who have expertise in specific investment areas. For entrepreneurs who understand certain markets deeply, this can be the perfect vehicle to leverage that knowledge for retirement security.

4. Low-Cost Index Solo 401(k)

For many self-employed individuals, simplicity and low costs are priorities when setting up 401k plans for self employed. The Low-Cost Index Solo 401(k) approach isn’t a different type of plan structure—it’s a smart investment strategy that focuses on passive investments with minimal fees.

This approach to solo 401(k) investing emphasizes broad-market exposure through index funds that simply track established market benchmarks like the S&P 500 or total stock market indexes. The beauty lies in its simplicity and cost-effectiveness.

“The magic of compound interest is powerful, but investment fees can silently erode that magic over decades,” explains one retirement planning expert. “For self-employed individuals managing their own retirement, minimizing these costs can add six figures to your retirement balance.”

What makes this approach so appealing is the combination of zero setup fees at many providers, streamlined paperwork, and annual expense ratios typically under 0.20%—compared to 1% or more for actively managed funds. Many platforms now offer commission-free ETF trading and even automatic portfolio rebalancing to maintain your target asset allocation without requiring constant attention.

The real-world impact is substantial. Consider two self-employed graphic designers who each contribute $20,000 annually to their solo 401(k) for 30 years, both earning a 7% annual return before fees:

- Designer A pays just 0.10% in annual fees and retires with approximately $1,818,000

- Designer B pays 1.00% in annual fees and retires with approximately $1,522,000

That nearly $300,000 difference comes solely from the impact of fees, not investment performance—it’s like giving yourself a massive retirement bonus simply by choosing lower-cost investments.

Most major brokerages now offer solo 401(k) plans with minimal administrative costs and access to hundreds of low-cost index funds and ETFs. This approach works beautifully for busy self-employed professionals who want to maximize their retirement savings while minimizing both costs and the time spent managing investments.

Stretch your contributions further

The impact of fees on your 401k plan for self employed individuals is like a slow leak in your retirement tire—barely noticeable day-to-day but devastating over decades. By minimizing these costs, you effectively give yourself a “raise” in retirement savings without increasing your actual contributions.

The math becomes even more compelling when you consider that a seemingly small difference in expense ratios—say 0.05% versus 1.25%—can translate to years of additional retirement income. With a low-cost index approach, you’re essentially capturing more of the market’s returns rather than handing them over to fund managers.

Most self-employed professionals find success with remarkably simple portfolios. A freelance photographer I worked with implemented a three-fund portfolio covering U.S. stocks (60%), international stocks (30%), and bonds (10%) with a weighted average expense ratio of just 0.06%. This approach required minimal maintenance while providing broad diversification.

Dollar-cost averaging is another powerful strategy that pairs perfectly with index investing. Rather than trying to time the market with lump-sum contributions, setting up automatic monthly transfers ensures you’re consistently investing regardless of market conditions. This removes emotion from the equation and creates a disciplined approach to building your retirement savings.

“I used to spend hours researching actively managed funds, hoping to beat the market,” shares one self-employed consultant. “Now my solo 401(k) is on autopilot with index funds. I spend that time serving clients instead, which actually increases my income and allows me to contribute more.”

Many providers now offer zero-commission trading on ETFs and even fractional share investing, allowing you to invest every dollar efficiently without having cash sitting idle. This means your money gets to work immediately rather than waiting until you have enough to purchase full shares.

When evaluating providers for your low-cost index solo 401(k), look beyond just the investment options to account fees, annual maintenance charges, and whether they offer features like automatic rebalancing. The most cost-effective plan is one that minimizes both investment and administrative expenses.

5. Solo 401(k) + Defined Benefit Stack

For high-earning self-employed professionals looking to boost their retirement savings, combining a solo 401(k) with a defined benefit plan creates what might be called the ultimate 401k plan for self employed strategy – the retirement savings equivalent of a turbocharger.

This powerful combination doesn’t just nudge your savings potential a bit higher – it can blast it into six-figure territory, allowing annual retirement contributions exceeding $100,000 in many cases. That’s far beyond what’s possible with even a maxed-out solo 401(k) on its own.

Here’s how this dynamic duo works together:

-

Solo 401(k): You contribute the maximum employee deferral ($23,500 in 2025, plus $7,500 catch-up if you’re 50+) and add the employer contribution (up to 25% of compensation)

-

Defined Benefit Plan: You establish what’s essentially your own personal pension plan with contributions determined by actuarial calculations based on providing a specific retirement benefit

The beauty of the defined benefit component is how it uses factors like your age, income, and years until retirement to determine your allowable contribution. The math works in favor of older business owners – the closer you are to retirement and the higher your income, the larger your potential contribution.

Consider Dr. Sarah, a 55-year-old self-employed dermatologist earning $300,000 annually. Her retirement stack might look like this:

– $31,000 to her solo 401(k) as employee contributions (including catch-up)

– $60,000 to her defined benefit plan

– Plus an additional employer contribution to her solo 401(k)

Her total annual retirement contributions could easily exceed $100,000, potentially saving tens of thousands in current taxes while rapidly building her retirement nest egg.

When stacking makes sense

Let’s be honest – this sophisticated retirement strategy isn’t for everyone. It’s like a finely custom suit rather than an off-the-rack option. The Solo 401(k) + Defined Benefit stack makes the most sense for self-employed individuals who fit a specific profile.

You’re likely an ideal candidate if you’re a high-income earner (typically bringing in $250,000+ annually) with stable, predictable income. This strategy particularly benefits older business owners (generally 45+ years old) who have fewer years until retirement. You should also have consistent profits since you’ll need to commit to several years of contributions.

This approach is perfect for self-employed professionals seeking maximum tax deductions during peak earning years and business owners planning an exit strategy who want to accelerate their retirement savings before selling or transitioning their business.

The defined benefit component does require more administrative effort. You’ll need to work with an actuary and typically face:

– Higher setup costs ($1,500-$3,000 to establish the plan)

– Annual administration fees ($1,500-$2,500 to maintain the plan)

– Required annual contributions based on the actuarial calculation

– Annual filing of Form 5500 regardless of plan size

But for the right person, these costs are mere pocket change compared to the tax savings and accelerated retirement funding. Imagine you’re a self-employed consultant in the 37% federal tax bracket who contributes $100,000 combined to these plans. You could potentially save $37,000 in federal taxes alone – not even counting state tax savings. Suddenly those administrative fees don’t seem so significant, do they?

This powerful stack works particularly well if you’re a late-start saver who needs to catch up on retirement funding after years of building your business. It’s also ideal if you’re having exceptionally profitable years and want to shelter that income, or if you’re a professional planning to work for 5-15 more years before retirement. The strategy is most cost-effective for those with few or no employees, as adding employees to the defined benefit plan significantly increases costs.

While it’s certainly more complex than simpler retirement options, this combination represents the pinnacle of retirement tax planning for high-income self-employed individuals. It’s like having access to a secret passage that can lead you more quickly to your retirement goals while keeping more of your hard-earned income out of the tax collector’s hands.

How to Open and Maintain Your Plan

Getting your 401k plan for self employed up and running doesn’t have to be complicated, but it does require attention to detail. Think of it as building the foundation for your financial future – worth doing right the first time!

Starting with the basics, you’ll need an Employer Identification Number (EIN) from the IRS if you don’t already have one. This is your business’s tax ID, and you can get it quickly through the IRS website. Next, take a moment to consider your business structure – whether you’re operating as a sole proprietorship, LLC, S-Corp, or something else – as this affects how you’ll calculate contributions.

One of the most important decisions you’ll make is choosing between traditional pre-tax contributions, Roth after-tax contributions, or a mix of both. This choice depends on your current tax situation and your expectations for retirement. Take your time with this decision – it’s about your financial future, after all!

“The most important step is simply getting started,” says one retirement planning expert. “Many self-employed people put this off because they think it’s complicated, but the tax benefits are too valuable to ignore.”

When selecting a provider for your solo 401(k), compare fees, investment options, and user experience. Some providers specialize in solo 401(k)s with streamlined paperwork and support specifically for self-employed individuals.

Once you’ve chosen your provider, you’ll complete their adoption agreement (the formal document establishing your plan) and set up the trust account that will hold your retirement assets. This needs to be done by December 31st if you want to make employee deferrals for that tax year!

For turning your retirement savings into reliable income later on, check out our detailed guide: How to Turn Your Retirement Savings into Reliable Income.

Step-by-step checklist

Setting up and maintaining your 401k plan for self employed becomes much easier with a clear roadmap. Here’s what you need to do at each stage:

Getting Started:

– Research providers carefully – fees and features vary widely

– Apply for an EIN at IRS.gov if you don’t already have one

– Select yourself as the plan trustee (typically)

– Complete and sign the adoption agreement by December 31

– Establish your trust account with your chosen financial institution

– Create a simple investment policy to guide your decisions

– Select initial investments aligned with your retirement timeline and risk tolerance

Annual Maintenance:

– Review the current year’s contribution limits (they adjust with inflation)

– Document your employee deferral elections before making contributions

– Make your employee deferrals by December 31st

– Calculate your allowable employer contributions (this differs for sole proprietors)

– Complete employer contributions by your tax filing deadline (including extensions)

– Rebalance investments to maintain your target asset allocation

– Review beneficiary designations to ensure they reflect your current wishes

Employee contributions (your salary deferrals) must be made by December 31st of the tax year, while employer contributions can wait until your tax filing deadline, including extensions. This gives you some flexibility in timing your contributions based on cash flow.

As your plan grows, you’ll need to monitor when your assets cross the $250,000 threshold, as this triggers the requirement to file Form 5500-EZ annually. This form is due by July 31st for the previous calendar year.

Common pitfalls to avoid in 401k plans for self employed

Even the most financially savvy business owners can stumble when managing their 401k plans for self employed. Being aware of these common pitfalls can save you headaches and potential penalties:

Missing critical deadlines is perhaps the most common mistake. Unlike IRAs, which allow contributions until tax day, employee deferrals to your solo 401(k) must happen by December 31st. New plans also need to be established by year-end if you want to make employee deferrals for that tax year. I’ve seen many disappointed business owners who waited until March to set up their plan, only to learn they missed the window for the previous year’s contributions.

Miscalculating contribution limits happens frequently, especially for sole proprietors. The calculation isn’t as straightforward as simply taking 25% of your business income. You need to use a special formula that accounts for self-employment taxes. If you have multiple businesses, things get even more complex, as contribution limits may be affected by your total self-employment income.

Hiring employees without adjusting your plan can create serious compliance issues. Once you hire someone who works more than 1,000 hours in a year, your solo 401(k) must either include them after they meet eligibility requirements or be terminated. With the SECURE 2.0 Act, this becomes even more important, as part-time employees working 500+ hours for two consecutive years will need to be included starting in 2025.

Sloppy recordkeeping can come back to haunt you. Keep copies of all plan documents, contribution records, and participant information. This becomes especially important if you’re ever audited by the IRS.

Forgetting Form 5500-EZ is another common mistake. Once your plan assets exceed $250,000, you must file this form annually by July 31st. You also need to file it when terminating your plan, regardless of asset size. The penalties for late filing can be steep – up to $250 per day with a maximum of $150,000!

Making prohibited transactions can disqualify your entire plan. This includes borrowing from the plan outside of proper loan provisions, using plan assets as security for a personal loan, or buying property for personal use with plan funds. The consequences can include immediate taxation of your entire plan balance plus penalties.

By staying vigilant about these potential pitfalls, you’ll ensure your solo 401(k) remains compliant while maximizing its benefits for your retirement future. After all, the 401k plan for self employed individuals is one of the most powerful wealth-building tools available to business owners – it deserves your careful attention!

Frequently Asked Questions about 401(k) Plans for Self-Employed

Who is eligible to start a solo 401(k)?

Wondering if you qualify for a 401k plan for self employed individuals? Good news—the eligibility requirements are pretty straightforward. You can establish one if you have self-employment income from a legitimate business (not just a hobby) and don’t have full-time employees besides yourself and your spouse.

This covers a wide range of independent workers including sole proprietors, consultants, freelancers, independent contractors, single-member LLCs, partnerships (where only partners participate), and corporations with only owner-employees.

Here’s something many people don’t realize—even if you have a full-time job with an employer 401(k), you can still set up a solo 401(k) for your side hustle. Just remember that your total employee deferrals across all plans can’t exceed the annual limit ($23,500 for 2025).

“I thought having part-time help would disqualify me, but that’s not always the case,” shares one small business owner. Part-time employees working less than 1,000 hours per year generally don’t affect your eligibility—though heads up, this is changing under SECURE Act 2.0, which will require long-term part-time employees to be included starting in 2025.

How are contributions calculated for sole proprietors vs. S-corps?

The way you calculate contributions for 401k plans for self employed individuals varies significantly depending on how your business is structured—and understanding the difference could potentially boost your retirement savings.

For Sole Proprietors, Partnerships, and LLCs taxed as such:

Your employee deferrals are straightforward—up to $23,500 in 2025 ($31,000 if you’re 50 or older). The employer contribution calculation is where things get interesting. It’s approximately 20% of your net self-employment income after deducting half of your self-employment tax and the employer contribution itself.

For example, if you have $100,000 in net self-employment income, you could make an employee deferral of up to $23,500 plus an employer contribution of about $18,587—for a total potential contribution of $42,087.

For S-Corporations and C-Corporations:

If you’ve structured your business as a corporation, you have a potential advantage. Your employee deferrals come from your W-2 wages (up to $23,500 in 2025 or $31,000 if 50+), and your employer contributions can be up to 25% of those W-2 wages.

With the same $100,000 in income, but now as W-2 wages from your S-Corporation, you could make an employee deferral of up to $23,500 plus an employer contribution of up to $25,000—for a total potential contribution of $48,500.

This difference is one reason many self-employed folks choose to operate as S-Corporations when their income reaches certain thresholds—it simply allows for higher retirement plan contributions compared to sole proprietorships at the same income level.

What happens if I hire a full-time employee later?

Many solo entrepreneurs worry about what happens to their 401k plan for self employed when their business grows enough to hire employees. It’s a valid concern, but there are several paths forward.

When an employee works 1,000 hours or more in a year (roughly 20 hours per week), they generally become eligible for your retirement plan. At this point, you have several options:

You could convert your solo 401(k) to a standard 401(k) that includes eligible employees, though this means complying with non-discrimination testing. Alternatively, you might choose to terminate the solo 401(k) and roll the assets to an IRA or new plan.

Many growing businesses opt for a Safe Harbor 401(k), which requires mandatory employer contributions but bypasses most testing requirements. Others switch to a different retirement plan entirely, such as a SIMPLE IRA or SEP IRA.

“When I hired my first full-time employee, I was worried about the paperwork nightmare,” shares a small business owner. “Working with a financial advisor helped me transition to a Safe Harbor plan that worked for everyone.”

The costs of maintaining your plan will increase with employees. You’ll likely need third-party administration services, compliance testing, additional recordkeeping, and potential employer contributions. Plus, Form 5500 filing becomes mandatory regardless of asset size, and you’ll need to provide plan disclosures to all participants.

Some small business owners choose to freeze their solo 401(k) (stop new contributions but maintain the existing balance) and establish a separate plan for the business with employees. This approach offers clean record-keeping and potentially simpler administration.

The good news? With proper planning, your retirement savings strategy can evolve right alongside your growing business.

Conclusion

401k plans for self employed individuals truly represent one of the most powerful financial tools available to independent workers today. If you’ve made it this far, you now understand how these specialized retirement plans can help you build substantial retirement savings while managing your tax burden in ways that employees of large companies might envy.

The beauty of these plans lies in your dual role – you’re both the employer and the employee. This unique position allows you to contribute significantly more than most other retirement vehicles would permit, potentially supercharging your retirement savings.

We’ve explored several powerful options throughout this guide – from the immediate tax benefits of the Traditional Solo 401(k) to the tax-free growth potential of the Roth version. We’ve looked at the investment freedom of Self-Directed plans, the cost efficiency of Low-Cost Index approaches, and even the turbo-charged potential of combining a Solo 401(k) with a Defined Benefit plan.

As you consider which approach makes the most sense for your situation, keep these essential takeaways in mind:

First, these plans offer remarkable contribution power. With the ability to save up to $69,750 in 2025 ($77,500 if you’re 50 or older), solo 401(k)s stand head and shoulders above most retirement options available to the self-employed.

Second, they provide incredible tax flexibility. The ability to choose between traditional and Roth contributions gives you powerful planning options that can be adjusted as your circumstances and tax situation evolve over time.

Third, depending on your provider, you’ll enjoy substantial investment freedom – from simple index funds that require minimal maintenance to alternative assets like real estate if you’re more hands-on with your portfolio.

Fourth, these plans offer relative simplicity in administration. Until your plan assets reach $250,000, the paperwork requirements are surprisingly minimal compared to other retirement plans.

Finally, these plans provide scalability as your business grows. Your solo 401(k) can adapt alongside your evolving business needs or be complemented with additional retirement strategies as your income increases.

At Finances 4You, we firmly believe that self-employed individuals deserve the same – if not better – retirement saving opportunities as corporate employees. The corporate world may offer stability, but the self-employed world can offer financial freedom when you leverage the right tools.

With thoughtful planning and consistent contributions, your solo 401(k) can help you build a retirement nest egg that provides the financial security and independence you’ve worked so hard to achieve.

For more insights on why starting your retirement planning journey today matters, check out our article on Why You Should Start Planning for Retirement Today. And don’t forget to explore our Business category for additional resources custom specifically to entrepreneurs and self-employed professionals like yourself.

The road to financial freedom isn’t built in a day – it’s paved with informed decisions and consistent action over time. Your future self will thank you for maximizing the potential of your solo 401(k) today.

5 thoughts on “No Employees, No Problem—Top 401(k) Plans for the Self-Employed”

Pingback: Retirement Planning Made Simple: Top 10 Ways to Prepare for Your Future - Finances 4 You

Pingback: One Simple Way to Optimize Taxes and Reduce Liability - Finances 4 You

Pingback: Finances4You: The Ultimate Tool for Personal Financial Success – Site Title

Pingback: How to Use Notion as Your Ultimate Finance Planner - Finances 4 You

Pingback: Money Matters When You’re the Boss: Financial Planning Tips for the Self-Employed - Finances 4 You

Comments are closed.